Following on from the content of our January 12 article, we have decided to take a closer look at the digital captive model. To do so, it is necessary to analyze and resolve some key issues that will optimize both its effectiveness and the user experience.

We would particularly like to focus on two important aspects: the fact that not all patients are the same and the definition of the products associated with the digital capitation model.

Understanding these points will allow you to understand the business rules that govern the model.

1. Risk segmentation: not all patients are the same

The traditional capita fixed a price per patient regardless of their clinical needs. This could encourage the provider to avoid complex patients, since they required greater dedication than stable or healthy patients. To correct this problem or bias, it is essential to make the capitated model more sophisticated through compensation mechanisms. In this way, the capita would become variable, adjusting to parameters such as age or state of health.

1.1. Age adjustment

The implementation of an age-based capita is straightforward, as it can be linked directly to the premium segmentation already used by insurers. In this scheme, the provider would receive an amount adjusted to the age of the assigned patient. However, the main drawback is that age alone does not guarantee that patients who require more intensive medical care are being adequately compensated.

1.2. Adjustment for health status

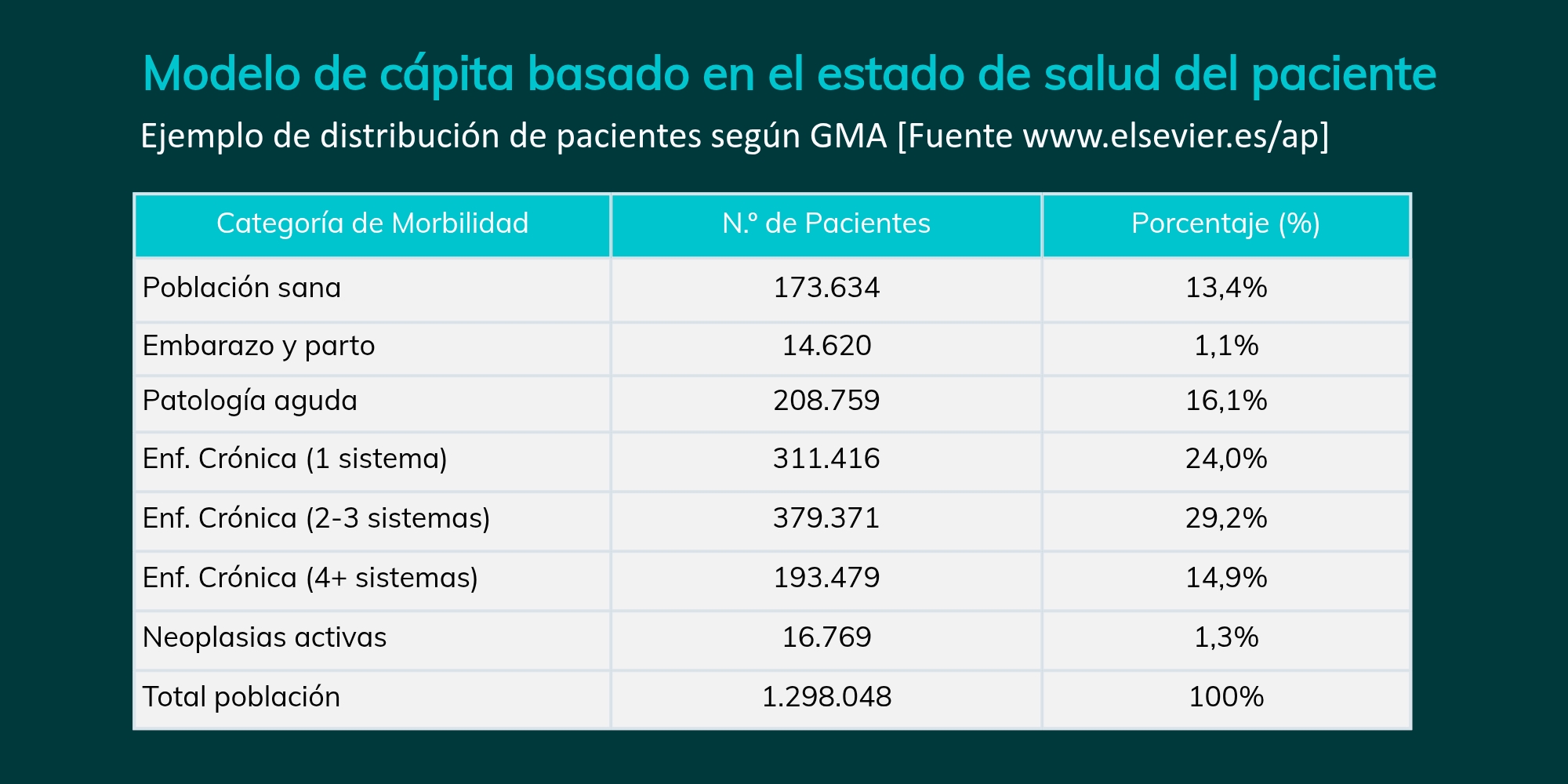

A capitated model based on patient health status is significantly more accurate and fair. Unlike the age criterion, this approach allows the population to be classified into specific clinical categories.

This classification can be self-designed or based on already validated methodologies, such as the Adjusted Morbidity Group (AMG). This system organizes patients into seven categories, also assigning five levels of complexity to each (except for the healthy population), which allows for a much finer actuarial adjustment.

Structure of the GMA model:

- Healthy population

- Pregnancy and/or childbirth

- Acute pathology

- Chronic disease in 1 system

- Chronic disease in 2 or 3 systems

- Chronic disease in 4 or more systems

- Active neoplasms

To illustrate the relevance of this parameter in the calculation of capita adjustments, we present a real example of population distribution according to the GMA model:

1.3. Initial cataloging and reevaluation

For the GMA-based model to be effective, our digital platform will manage the patient’s clinical classification in two critical phases:

- Initial Cataloging (Welcome Pack): An entry medical assessment will be performed to open the medical record and assign the risk category. Although it is possible to use the recruitment questionnaire, we recommend an initial clinical validation to ensure the accuracy of the capita from day one.

- Dynamic reassessment through AI: The system will periodically update the patient’s category by analyzing the CMBD reports. Currently, we have an AI prototype that processes the following diagnoses ICD-11 diagnoses in each consultation to automate this complexity adjustment under medical supervision.

1.4. How to promote the doctor-patient relationship

A relevant aspect of the model is to prevent the fixed payment from discouraging healthcare activity or limiting the clinical relationship to the patient’s initiative in the face of a health problem. To minimize this effect, business rules are proposed such as:

- Annual renewal of the capita: Payment will be conditioned to an annual review and follow-up visit, where the physician will be required to complete a health test. This service would be paid as an additional incentive; without this evaluation, the monthly payment of the capita would be suspended.

- Mandatory initial consultation: An initial consultation (preferably by video call) with each newly assigned patient is required to assess their health status and present the available prevention plans, even in healthy patients. The formalization of this plan, which includes the initial recording of the medical history (history, allergies, etc.), would be a prerequisite to start receiving the capita and could be associated with an economic incentive.

2. Products associated with the digital capitative model

As mentioned, this model is optimal for high frequency and low clinical intensity specialties. Its implementation is projected in three main product typologies:

2.1. Types of products

- Personal Medicine and Healthy Living Plans: Reduced premium products aimed at young people and people interested in healthy habits. They integrate preventive and wellness services, such as gyms or personal trainers.

- Insurance for Seniors: Conceived as a specific or complementary product. Here, the assigned physician acts as health manager and counselor, coordinating referrals to specialists. The model provides a premium bonus for those patients who adhere to this guided care scheme.

- Complement to Traditional Insurance (Family Doctor): The doctor assumes the integral management of the family health (ideally, the same professional for the whole family). This role includes prescriptions, tests and controlled referrals. This approach reduces the dispersion and duplicity of expenses generated by uncontrolled access to the medical directory, improving the control of the insurance risk and, therefore, the premium.

2.2. Key specialties for implementation

Encouraging the assignment of trusted (favored) physicians who manage family health holistically improves user experience and cost efficiency. The most appropriate areas are:

- Primary Care / Family / Personal Physician.

- Pediatrics and Gynecology.

- Psychology and Podiatry.

- Wellness and healthy living plans.

2.3. Flexibility and telemedicine

The assignment of the physician is always the patient’s decision, and the patient may change his or her choice at any time. This choice can be:

- Express: By direct action of the user.

- Implicit: By means of an algorithm that automatically assigns the professional according to the insured’s history of use (favorite doctors).

It is important to note that the assigned physician does not necessarily require a physical presence nearby. The model allows for delocalization, making special sense when the professional has specific expertise (sports medicine, dietetics, etc.) that is of interest to the insured. Through our online care platform, telemedicine guarantees quality clinical management regardless of geographical location.

3. Conclusion

In essence, this model proposes a profound transformation in the behavior and operations of all those involved. For the patient, it guarantees immediate and personalized access to services, while preserving the patient’s freedom of choice. For the professional, it shifts the focus from the generation of medical acts to proactive, health-centered follow-up. Finally, for the insurance company, it represents a leap in risk control through precise knowledge of the state of health of its policyholders.